New + updated

The 12 Best Snowboard Brands of 2024

March 4th

There’s no denying that our every day lives are expensive. From rent to groceries, the list of expenses goes on and on. Sigh. And for big ticket items, like furniture or a new car, it can be tough to save up the cash to make the purchase outright. There are a number of factors that will influence your purchase options such as a low income, high costs of living, or large amounts of debt. In this guide, we’ll explore which buying option suits you best: buy now pay later vs credit cards.

What Is Buy Now Pay Later?

Folks, it’s as easy at it sounds. Buy now, pay later (BNPL) is a financing avenue that allows shoppers to buy something but pay for it later. The payment is done within a stipulated interest-free time period in three or more installments. There are certified BNPL providers that settle the bill with the sellers outright.

Who Is BNPL for?

While anyone can avail these schemes, the targeted demographic for this purchasing option is cash-strapped millennials. Hits too close to home, right? Basically, if you’re young, new-to-credit, and don’t have credit cards, BNPL is the perfect way to buy what you want.

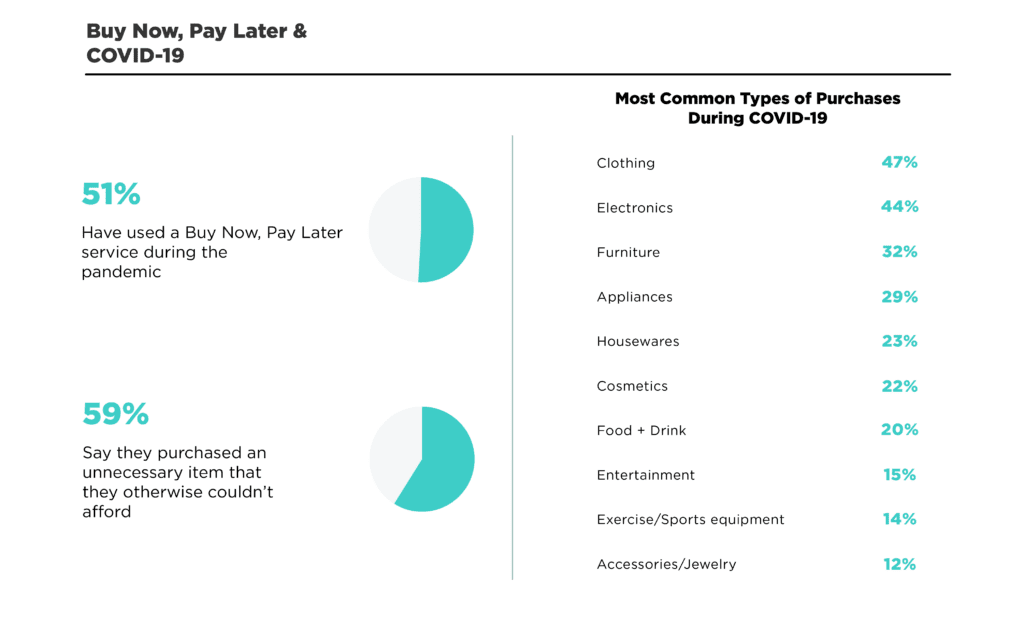

What Can You Buy With the Paying Later Option?

Since more and more millennials are flocking to cashless transactions, BNPL is available for a huge variety of items! Have a look below:

What Is the Difference Between Credit Card and BNPL?

With a credit card, you have the option to convert your purchase into equated monthly installments (EMIs) spanning over several months, usually up to 12 months. Sometimes, it can be as long as 3 years. This lets you pay for your purchase in smaller installments, which makes it more manageable financially.

Buy Now Pay Later vs Credit Cards: Interest-Free Period

Most credit cards offer an interest-free credit period of up to 45 days. Buy now, pay later, offers a shorter interest-free credit period of up to 15 days.

However, some BNPL lenders offer up to 45 days of this interest-free period.

🛍️ Related: 8 Common Coupon Codes in 2022 To Try

Choose Your Purchasing Option: Buy Now Pay Later vs Credit Cards

Buy Now Pay Later

| PROS ✅ | CONS ❌ |

| No Hard Credit Check: Many, but not all, BNPL providers don’t perform a hard credit check when you open an account. However, some of them will perform a soft credit pull, which doesn’t impact your credit score in any way! Therefore, it’s easier than qualifying for a credit card. | Late Fees: If you forget to make a payment or don’t have enough funds in your linked bank account, you may be charged late fees. While many of them are reasonable flat-rate fees in line with those assessed by credit cards, these can add up over time. Therefore, it’s best to pay your dues on time. Also, be careful of deferred interest promotions. If you don’t pay off the balance in full by the end of the promotional period, you’ll be hit with interest from the original purchase date. |

| Interest-Free Periods: BNPL can be a good deal if you take advantage of the interest-free period and pay off your balance on time. You’ll be able to receive your purchase right away and pay for it over time without having to pay any interest! | Small Credit Limits: There are a variety of BNPL providers, each with their own credit limit. Some are for smaller purchases of a few hundred dollars, while others can run up to a couple of thousand. If you have good credit and a healthy income, you’re likely to get a higher credit limit with a credit card. |

| Fast and Convenient: BNPL options allow you to shop without having to fill out any separate applications or wait for processing to complete. The payment options are integrated with many online retailers, so it’s easy as one, two, three. | BNPL Doesn’t Build Credit: If you’re looking to build credit history with on-time payments, BNPL avenues aren’t the best way to go. Most of these apps don’t report your payments to the credit bureaus, so your credit score won’t increase. |

This is your checkpoint to assess your spending habits and not get carried away by the ease and breeze of paying later. Trust us, your future self with thank you.

Credit Cards

| PROS ✅ | CONS ❌ |

| Build Credit Rating: Your credit card account details and payment history are important factors in your credit score. If you keep your account in good standing, this will help you build a good credit score. This could then increase your chances of approval for other products such as car loans or a mortgage. | Credit Damage: If you don’t make your credit card repayments, or have other outstanding debts, this information is recorded on your credit file. This can impact your ability to get a loan in the future. |

| Emergency Line of Credit: Credit cards can be a lifesaver if you don’t have enough cash or savings to cover an unexpected cost. Just remember that you’ll need to pay back everything you owe. | High Rates of Interest: If you carry a balance on your credit card from month-to-month, you’ll pay interest charges. The purchase and cash advance interest rates can be as high as 22% APR, which means you can end up paying hundreds or thousands more than you initially charged in interest if you’re unable to make repayments each month. |

| Work in Any Currency: If you have a credit card that doesn’t charge for currency conversion, then using it overseas is a great way to save money. This could come in handy if you do a lot of online shopping or are planning a holiday abroad! | Annual Fees: Most credit cards come with annual fees. Annual fees can range from as little as $25 to as much as $1,200, depending on what type of card you have. Generally, the more features and perks you want on your card, the higher the annual fee will be. |

🛍️ Related: Online Shopping Safety Tips: 9 Ways To Protect Yourself from Cyber Threats!

In Conclusion

While both options – buy now pay later vs credit cards – have their merits and drawbacks, it’s ultimately up to you what you’re comfortable with. If you’re looking to shop causally for items that are beyond your reach at the moment, then BNPL is a great option! However, if you’re thinking long-term and want to build credit, you might want to consider credit cards.